Disability Insurance

When You Can't Work, Disability Insurance Goes To Work For You.

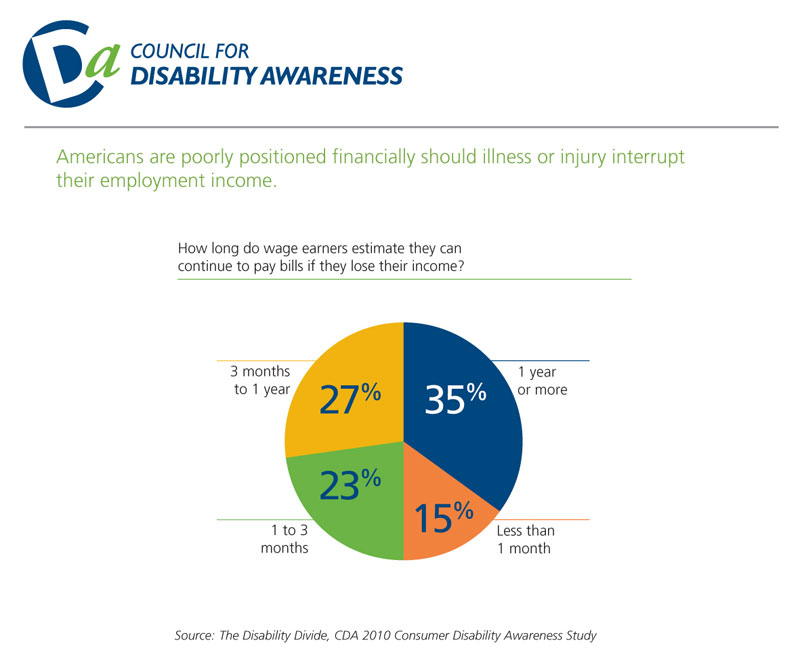

But what would happen if you become disabled or ill and could not work?

How would you...

- Pay your bills?

- Make your monthly rent or mortgage loan payments?

- Buy your groceries?

- Make your car payments?

- Provide for your children’s education?

- Save for retirement?

Most people don't realize the risk of becoming disabled, permanently or temporarily, at some point in their lives. But the reality is that at age 40, your chances of becoming disabled for 90 days or more prior to age 65 is 43%. (Source: 2004 Field Guide, National Underwriter)

When evaluating the chances of disability, you should carefully consider sources of available funds:

- Employer coverage - How long would the business continue to pay you? How much would they pay you? When would your employer have to hire a replacement? Could the business afford to pay both?

- Using savings - If you saved 10% of your income each year, one year of total disability could wipe out 10 years of savings. Can you afford that?

- Obtaining a loan - Without an income, who will lend you money?

- Working Spouse or Partner - Can your spouse or partner earn enough and be a companion, parent, private nurse, and employee - all at the same time?

- Selling investments - Will a sale under forced conditions bring a true value? What will their value be at the time you are disabled?

- Collecting Social Security - You cannot collect benefits until the end of the fifth full calendar month of total disability and only if it is expected to last 12 months or more. What will you do if your disability doesn’t meet those requirements? Even if it does, can you wait six months for payment?

- Counting on friends, family or charity - Would these sources have funds for you to use? Do you want to depend on them?

Many different disability insurance products are available to help protect you and your family against severe financial hardship that may accompany a disability.